The “Bank in a Box” BaaS Revolution: Banking-as-a-Service

Imagine this: You walk into your favorite coffee shop. You pull out your phone to pay, but instead of opening a generic banking app, you open the coffee shop’s app. You scan a QR code, pay with a debit card branded with the shop’s logo, and instantly earn 5% cashback on your latte.

Behind the scenes, you didn’t just buy coffee; you interacted with a fully functional bank account embedded right inside a loyalty app.

Welcome to the world of Banking-as-a-Service (BaaS). It is the invisible magic that allows non-banks—from ride-sharing giants like Uber to software startups to act like financial institutions without ever needing to wear a suit, visit a regulator, or build a vault.

Here is how the “Lego blocks” of modern finance are letting anyone build a bank, and why it is becoming the hottest trend in tech.

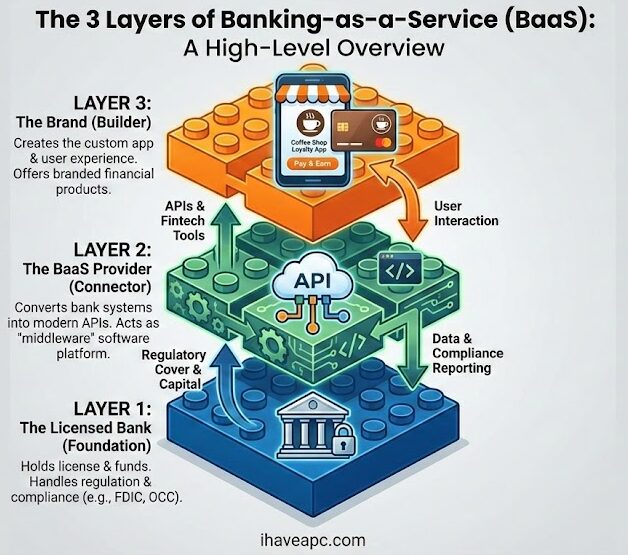

What is Banking-as-a-Service (BaaS)? (The “Lego” Analogy)

Traditionally, becoming a bank was incredibly hard. You needed millions in capital, a distinct banking charter, and years of regulatory approval. It was an exclusive club with a very high bouncer at the door.

BaaS changes the rules. Think of it like a set of Legos.

The Licensed Bank (The Foundation): These are regulated institutions (like Green Dot, The Bancorp Bank, or specialized partner banks) that hold the actual banking license. They handle the scary stuff: compliance, holding the money, and talking to regulators.

The BaaS Provider (The Connectors): These are tech platforms that connect to the bank’s clunky, old-school systems and convert them into modern, easy-to-use software code (APIs).

The Brand (The Builder): This is the startup, the retailer, or the gig-economy app. They take those APIs (Legos) and build a cool, branded financial product for you.

Because of this three-layer cake, a software company can launch a checking account in weeks, not years.

Why Is Everyone Doing It?

It’s not just about looking cool. It’s about “Stickiness.” If a software company manages your business operations and holds your money, you are much less likely to leave them for a competitor. Plus, they make money on every swipe of that branded debit card (called interchange revenue).

1. White Label Banking as a Service: Your Brand, Their Engine

When we talk about white label banking as a service, we are talking about the ultimate makeover.

In the old days, if a company wanted to offer a card, they would just slap their logo on a generic bank card (co-branding). White label BaaS goes much deeper. It allows a brand to control the entire user experience (UX).

- The “Invisible” Bank: The user logs into your app, sees your colors, and talks to your customer support. They might never know that “Bank XYZ” is actually moving the money in the background.

- Custom Cards: You can issue physical or virtual debit cards that are fully customized.

- Niche Features: You can build banking features that a traditional bank would never dream of.

Example: A banking app specifically for freelancers that automatically sets aside 30% of every deposit for taxes. A generic bank wouldn’t do that, but a white-label BaaS solution allows a startup to build exactly that logic.

Companies like Marqeta have revolutionized this space by allowing companies to issue cards that are incredibly smart—like a delivery driver’s card that only works at the specific restaurant they are picking up food from, and only for the exact dollar amount of the order.

2. BaaS Platforms for Startups: The Middlemen Making It Possible

If you are a startup founder, you don’t want to call a 100-year-old bank and ask for API access. You want a dashboard. This is where BaaS platforms for startups come in.

These platforms act as the “middleware.” They have already done the hard work of integrating with the banks. They resell that access to startups in a way that is developer-friendly.

Who are the key players?

- Stripe Treasury: Known for payments, Stripe now allows platforms (like Shopify) to offer bank accounts to their merchants.

- Unit & Treasury Prime: These are heavy hitters in the startup world. They focus on making the connection between the tech company and the bank seamless, handling much of the complex compliance monitoring automatically.

- Starling (Engine) & ClearBank: In the UK and Europe, these players are actual banks that built their own tech stacks from scratch to serve other fintechs.

The “Speed to Market” Advantage: Using these platforms, a startup can go from “idea” to “issuing our first debit card” in a matter of months. In the traditional banking world, that timeline would be 18 to 24 months.

3. Embedded Lending Infrastructure: The Real Money Maker

Checking accounts are great for engagement, but embedded lending infrastructure is where the profit is.

“Embedded lending” is just a fancy way of saying: Offering a loan exactly when the customer needs it, without making them go to a bank.

- Buy Now, Pay Later (BNPL): You’re at the checkout buying a $200 jacket. A popup offers to split it into four payments. That is embedded lending.

- Merchant Advances: Imagine you run a business on Amazon or eBay. The platform sees your sales data. They know you are good for the money. So, they offer you a $10,000 instant loan to buy inventory, deducted automatically from your future sales.

- Why it wins: Traditional banks require paperwork and credit checks that take weeks. Embedded lenders use real-time data (like your sales history on the app) to approve loans in seconds.

According to a report by McKinsey & Company, embedded finance (which includes lending) could be worth hundreds of billions in value, simply because it captures the customer at the point of sale.

The Reality Check: Compliance is Not Optional

It sounds fun and easy, right? Build a bank, issue cards, profit!

However, the “BaaS” industry faced a reality check in 2024 and 2025. Regulators (like the FDIC and OCC in the US) started looking closer at these partnerships. They realized that while the startup owns the customer relationship, the bank is still responsible if money is laundered or fraud occurs.

The “Sponsor Bank” Bottleneck:

Because of this, banks are becoming pickier about who they work with.

- KYC (Know Your Customer): You cannot just onboard users anonymously. Even if you are a cool crypto startup, you must verify identities.

- AML (Anti-Money Laundering): Your BaaS provider must have rigorous software to catch bad actors.

If you are building a BaaS product today, you aren’t just building software; you are building a compliance culture. The platforms that succeed are the ones that take this seriously, rather than just “moving fast and breaking things.”

The Future: Everything is a Bank

We are moving toward a future where “banking” isn’t a place you go, but a thing you do usually inside another app.

- Your property management app will hold your security deposit.

- Your car’s dashboard will have a wallet to pay for gas automatically.

- Your freelance job board will advance your pay before the client even sends the check.

By leveraging white label banking, BaaS platforms, and embedded lending, companies are dissolving the barriers between “buying something” and “banking.”

For the consumer, it means less friction. For the startup, it means new revenue streams. And for the industry, it means the definition of a “bank” has changed forever.

Ready to Build?

If you are considering integrating financial services into your product, start by identifying the specific “financial pain” your user has. Do they need faster access to funds? easier ways to pay expenses? Once you know that, you can choose the right BaaS provider to help you stack those Legos.

Happy banking.

Why Going Analog in 2026 is the Ultimate Power Move

Sustainable Tech: The Resale Value of 2026 PC Components